Self employed workers without child dependants will get no payment under Universal Credit.

Huge cuts to Tax Credits

These have been concealed in Universal Credit legislation and passed in the Welfare Reform Act 2012/13 These changes are due to be implemented from April 2015 and HMRC have begun the process with new rules issued last month.

Worst hit are the self employed

They will get nothing under Universal Credit (UC) if they have no dependant children and those with children face cuts to the money they do receive. These are workers who would be eligible for Working Tax Credit, but changes under UC to the Work Allowance and the application of a ‘minimum income floor’ (MIF) to the self employed will make many ineligible.

The combination of the Minimum Income Floor(1) and the Universal Credit Work Allowance(2) mean that claimants will lose some UC if they have dependants and all if they don't.

50% reduction in income entitlement levels under Universal Credit

Work Allowance cut from £9,850 for Working Tax Credit to £1332 under Universal Credit for claimants without child dependants

Under Universal Credit, the level of earnings allowed before benefits are reduced is half that of Working Tax Credit for claimants without dependants (fig.1).

Under Universal Credit, the level of earnings allowed before benefits are reduced is half that of Working Tax Credit for claimants without dependants (fig.1).

The Minimum Income Floor

Under UC, self employed claimants are subject to a Minimum Income Floor (MIF), which,

if they fail to earn it, will be treated as ‘notional earnings’ and their UC payments are calculated as if it had been earned. The UC Work Allowance is then applied to these ‘earnings’. The Work Allowance is set at a low level for workers without dependants, so if they actually earn the MIF, they will not receive payments and for those with one dependant child, payments are reduced.

Universal Credit payments

Workers with no dependants have a Universal Credit award of £314/month (£494.95 for a couple). These payments are clawed back by 65p for every extra pound earned above a ‘Work Allowance'(2) which varies according to circumstances. This means the Universal Credit payments reduce to zero above a certain level of income.

Self-employed workers with no dependants get nothing

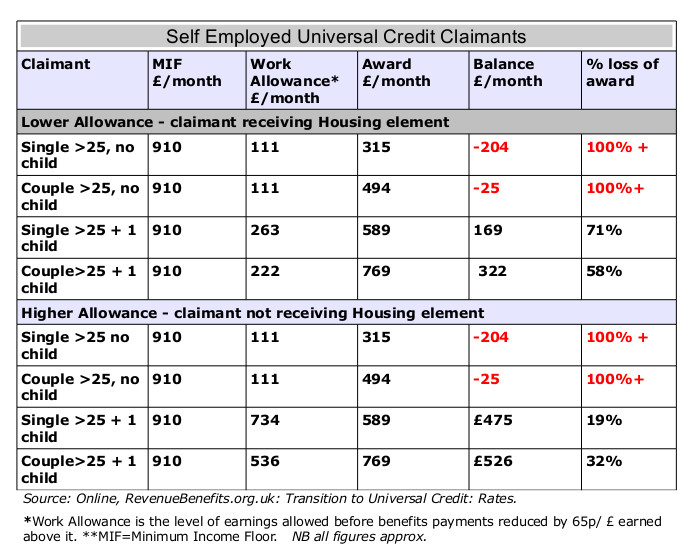

There is a catch for self-employed workers. Unless they earn more than the “Minimum Income Floor”(1) their income for UC purposes is assumed to be the MIF figure. This is currently £910 per month.

The further catch is that for self-employed workers without dependants, the Work Allowance is £111 per month. This is so low that, when their income is assessed to be at the level of MIF (£910 per month), the claw-back is £519.35p and exceeds their UC allowance. This means they receive no Universal Credit payments.

Self-employed workers with dependants get less.

For self-employed workers with dependant children, basic award payments could be reduced by up to 71% for a single parent (lower rate Work Allowance) and up to 58% for a couple (lower rate Work Allowance). See table 1.

All low paid workers will be subject to conditionality and sanctions,

However, employees, unlike self employed claimants, are not subject to the MIF, so will receive a tapering amount of UC as their earnings increase below the MIF level. But, for self employed claimants who fail the ‘gainful self employment tests’ (including the MIF), may be forced to abandon their businesses in order to survive and sign up to Jobseekers.

Note 1: The ‘minimum income floor’ (MIF) is the equivalent of 35 hrs/wk at the minimum wage, just below £11,000 (£910 per wk) which Self employed claimants should earn as UC ‘will not bridge that gap’ Of 4.5 m. self employed workers in the UK, 36.6% earn less than the £11,000/yr.

Note 2: The UC Work Allowance is the amount of money a claimant can earn before their UC is reduced and there are different rates for different claimant categories and these are set in the Welfare Reform Act 2013. UC is cut by 65p in every £ earned by claimants above the Work Allowance.

References

1. The Universal Credit Regulations 2013 No. 376 Part 6 Chapter 2 Gainful self-employment Regulation 62 http://www.legislation.gov.uk/uksi/2013/376/regulation/62/made

2. The Universal Credit Regulations 2013 no. 376 Part 3 Regulation 22 Deduction of income and work allowance: http://www.legislation.gov.uk/uksi/2013/376/regulation/22/made

DISCLAIMER: All content provided on this blog ‘Makingworkerspay’ is for information purposes only. The owner makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information.